Frozen and Refrigerated Cold Chain Insights

The Cold Front, presented by RLS Logistics, the Cold Chain Experts, is a monthly summary highlighting pertinent cold chain market data in one concise location. We proudly offer nationwide cold storage warehousing, less than truckload shipping, truckload transportation and eCommerce fulfillment cold chain solutions. As cold chain experts in frozen and refrigerated logistics, we are focusing on these topics for our November 2020 issue: reefer spot rates, reefer market conditions, and the diesel outlook. These insights ensure that you have the data you need to make better decisions to fuel your growth. We hope you find this information useful! If you would like data on your specific market, click the link below.

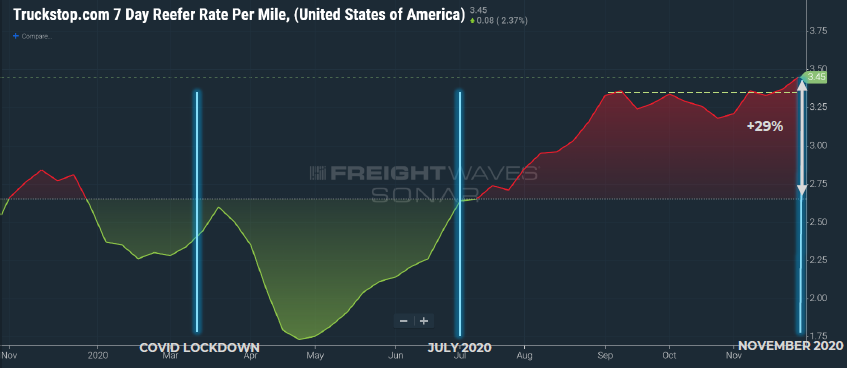

Reefer Spot Rates

Reefer spot rates continued to climb in November. Holiday volumes pushed spot market rates to their highest level for the trailing 12 months and increased 8.5% since the October 2020 edition. Compared to November 2019, rates have increased by 29%. Green shaded areas indicate relatively loose reefer capacity where shippers realize lower rates. The red shaded areas indicate tight capacity and significantly higher transportation rates.

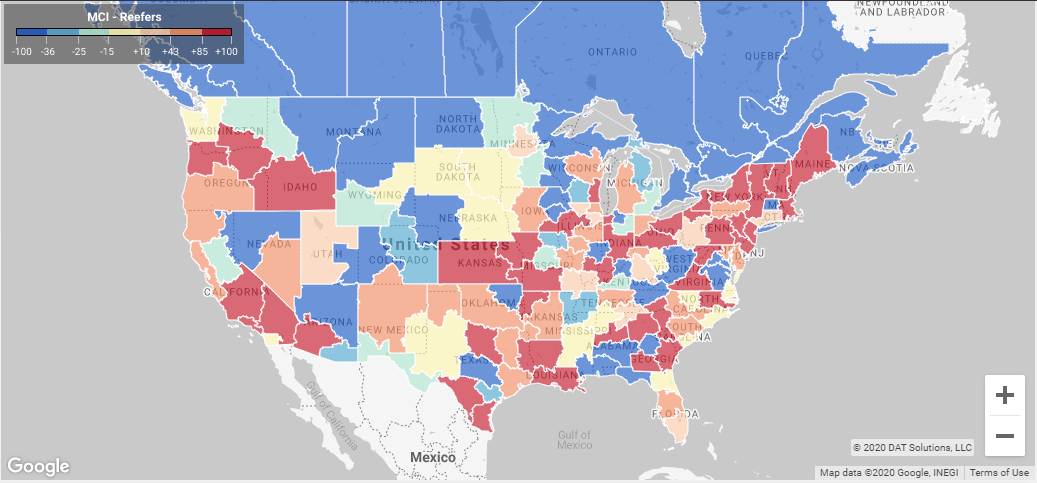

Reefer Market Conditions

The November 2020 freight market map below indicates some changes from October in the New England and Southeast markets, indicating tight capacity, demanding higher prices. Blue areas signify looser capacity while areas orange to red suggest a high load to truck ratio. Midwest and areas of Texas have cooled off from the previous month. New Mexico to Southern CA have also shown signs of cooling off, but capacity remains tight in those markets.

Diesel Outlook

The demand for diesel fuel has increased nationwide since the spring and summer. DOE national diesel prices increased $0.04 per gallon last week and have been on the rise the past four weeks. The national average price per gallon for diesel was $2.502 per gallon, marking the first time since April 13th that diesel’s price has been above $2.50 per gallon. With the hope of a COVID-19 vaccine, a reduction in global oil inventories, coupled with an increase in maritime demand, indicates higher oil futures. We will keep an eye on oil and diesel prices as we move into 2021.